Contribution from Gibran Registe-Charles, CEO/Founder, Urban Edge Capital

ESG is one of the most discussed topics across the investments landscape today.

There has been a significant growth in funds that incorporate ESG principles in their investment decision-making. According to Morningstar Direct, global ESG fund assets increased to $2.74 trillion in December 2021, up from $1.65 trillion at the end of 2020 and $1.28 trillion at the end of 2019 (30 ESG And Sustainable Investing Statistics (July 2022 Update) – SustainFi).

But there is no doubt that ESG is controversial. Fundamental traditional growth managers, whose portfolio includes big tobacco, munitions, and heavy mining companies, have seen consistent growth through investment in these businesses over the last two decades. These managers don’t implement negative screening and see ESG as clever marketing.

On the other hand, some ESG managers whose negative screening of pornography, alcohol, tobacco, and weapons (so-called “sin stocks”) have seen their ESG portfolios out-perform their cohorts.

According to McKinsey’s “Five ways that ESG creates values” report, companies with a strong ESG mandate see higher equity returns from both a tilt and momentum perspective, and ESG does not experience a drag on value creation either.

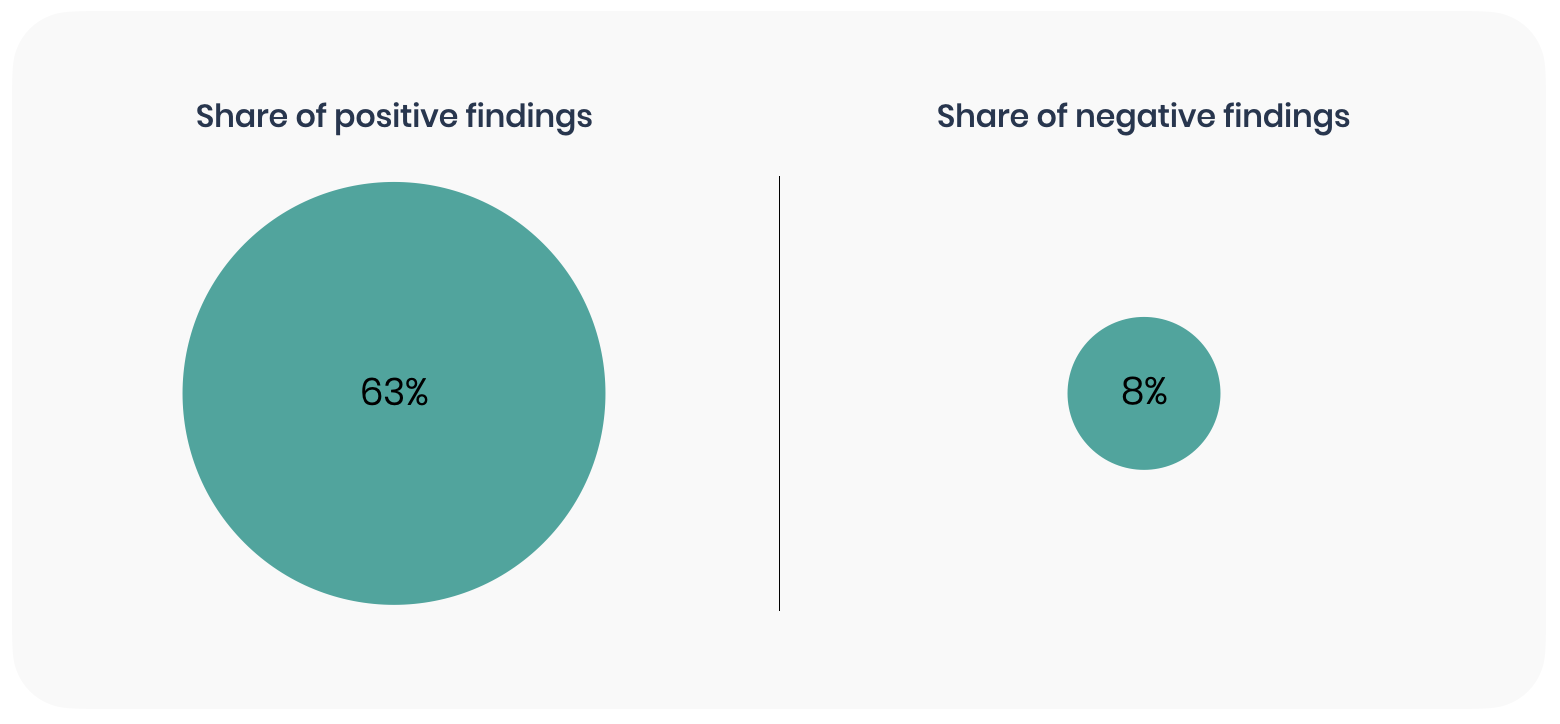

Paying attention to environmental, social, and governance (ESG) concerns does not compromise returns – rather, the opposite.

Results of > 2,000 studies on the impact of ESG propositions on equity returns

Source: Gunnar Friede et al., “ESG and financial performance; Aggregated evidence from more than 2000 empirical studies,” Journal of Sustainable Finance & Investment, October 2015, Volume 5, Number 4, pp.210-33; Deutsche Asset & Wealth Management Investment; McKinsey analysis

Naturally, this depends on the position in the ESG trifecta. Valuation specialists like to be neutral and class companies as either good or bad – good companies being ones that are sensitive to emissions and climate wellbeing, and considerate to socio-economic situations along with strong governance. The evidence is overwhelming to prove that there is something to discuss, and according to Bloomberg ESG report the market is set to grow to $50 trillion by 2025.

In 2020, there were 905 alternative ESG funds, including hedge funds, private equity, venture capital, REIT, and property funds, increasing from 780 in 2018.

But while the trend is upwards, there are still some challenges to adoption:

- Lack of evidence that ESG investments generate better returns. While there are claims that organisations managing ESG risks better have higher return potential in the long run, adequate evidence is not present to get to a market wide consensus.

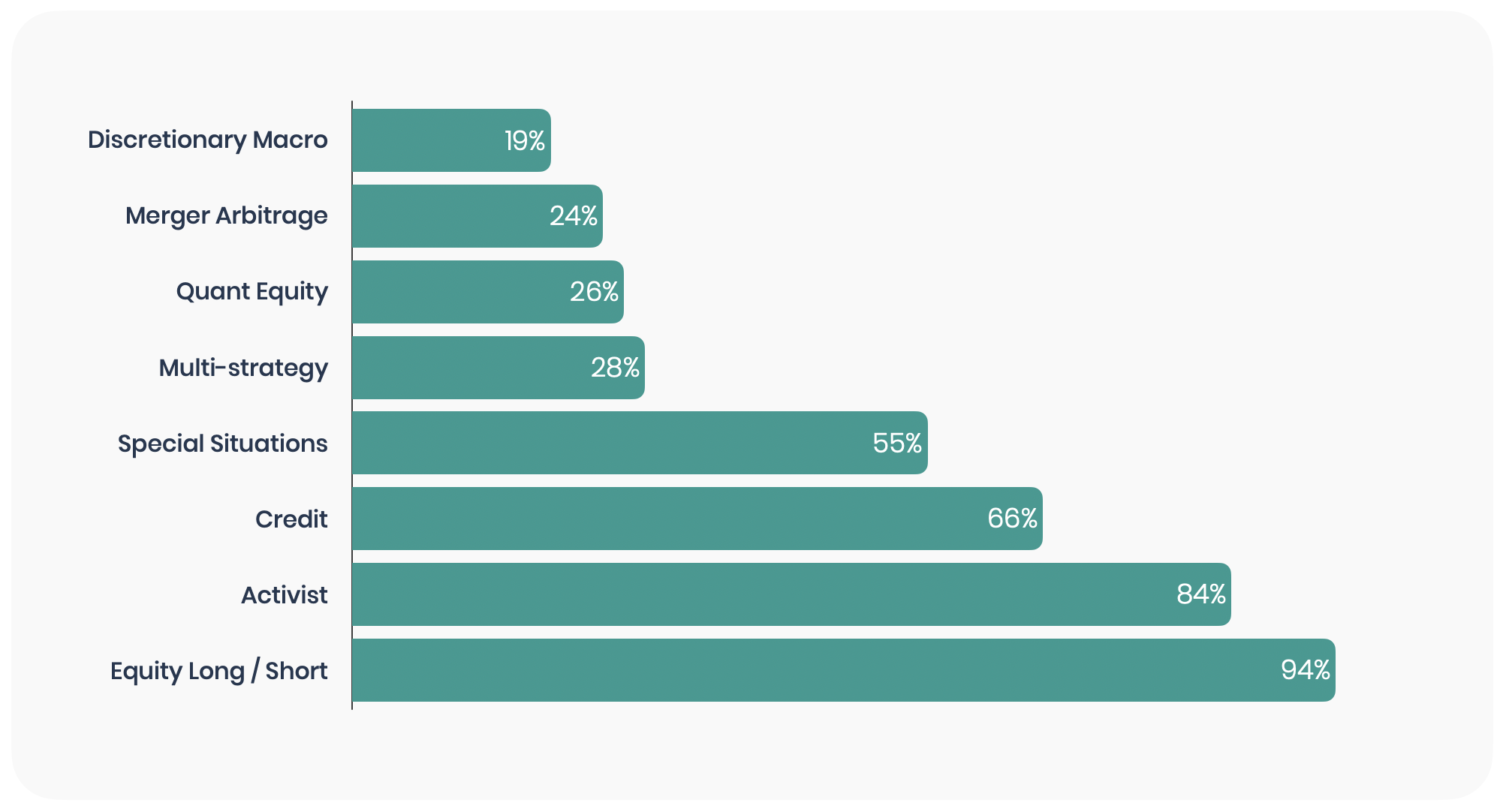

- Investment strategies in the hedge funds space do not align – for example, most hedge funds trade at macro levels including currencies, FX, and commodities. Equally, several strategies have a shorter-term time horizon. Investors do see opportunities to incorporate ESG principles into certain strategies:

Do investors believe ESG can be integrated across strategies?

Source: HFR, Barclays Strategic Consulting Analysis, April 2021

- Data challenges with sourcing and integrating ESG data sets, primarily in the private asset classes. This space is continuing to grow as well with various disclosure requirements such as Corporate Sustainability Reporting Directive, which affects 50,000 companies as it seeks to strengthen and standardise corporate EU ESG disclosures for better transparency, consistency, and comparability.

During the first half of 2022, BNY Mellon | Pershing’s Capital Introductions team surveyed 70 investors about their true ESG objectives (ESG Exuberance is at All-Time Highs. But Will Investors Buy? – BNY Mellon | Pershing), and the results indicate that we still have a way to go before there is true allocation.

Of those surveyed, only 4% were allocating to ESG strategies today via asset allocation buckets. That means 96% were not investing in ESG in a formal way, which is the biggest indicator of where the actual demand for ESG strategies is currently. In addition, 30% of investors shared that they allocate to ESG strategies opportunistically, which is further evidence of a slower pace of ESG adoption.

Another reason for this uncertainty is that, along with inconsistent ESG vendor scores, many larger houses are unsure of their position and are gradually hiring ESG managers to help navigate the myriad of opportunities available. Most governing regulators, including the FCA, are now issuing mandatory ESG policies for firms seeking additional investor support to ensure they meet ESG requirements on carbon footprint, diversity and inclusion, and governance.

While the true adoption may still be in the nascent stages, ESG investing continues to gather momentum. As this trend continues, organisations will need to focus on their ability to seamlessly integrate and utilise new ESG data sets in the investment decision making as well as reporting process.

A flexible nimble platform able to meet evolving requirements will certainly add value to organisations as they enter the fray. We look forward to partnering with clients and investors to navigate this evolving landscape and embed ESG considerations into their portfolios.